larifying further, the expectations projected by direct or indirect stakeholders onto an online shop run by a brand manufacturer with existing sales channels, versus a pure play newcomer, are fundamentally different. This is not even touching on the fundamental differences in doing e-commerce as a retailer such as Amazon, versus a brand manufacturer like Rolex.

Having a history in the luxury and sporting goods industries, I have seen nervous CEO’s plugging millions into their e-commerce activities for two main reasons; the success of online marketplaces in their respective industries, and the rise of direct brands taking market share.

Surprisingly, the CEO’s rarely reflect on why online marketplaces are able to disrupt their RRP pricing, and furthermore how direct brands have the opportunity to out spec and out price the traditional players through an online pure play approach. Unfortunately traditional brands have no real answer, however the upside is that the losses incurred by these new market entrants are fuelled by investors money, which provides much needed time to change a consumers buying habits.

Due to CEO’s not knowing what to do, they hire a multitude of e-commerce staff, mostly coming from retail and who have little to no understanding of a brand manufacturer’s supply chain, after-sales service structure or trade habits. They set out to create an online shop that according to the annual shareholder meetings, shows growth year-over-year by several 100% (from 1 piece to 3 pieces sold = 300% ;-), whilst pissing off their existing trade partners, the brick and mortar retailers and importers supporting the retailers. These retailers & import partners are quite rightly ticked off by the unthinking actions of the brand manufacturer’s new commerce experts, who then request the brand to enter into consignment deals. Slowly and invisibly over time the ecommerce strategy transfers all inventory risk onto the brand manufacturer’s balance sheet, thus exposing the business to a centralised pure play state, but with the cost structure of a bloated traditional retail machine.

Surprisingly, the CEO’s rarely reflect on why online marketplaces are able to disrupt their RRP pricing, and furthermore how direct brands have the opportunity to out spec and out price the traditional players through an online pure play approach.

These retailers & import partners are quite rightly ticked off by the unthinking actions of the brand manufacturer’s new commerce experts, who then request the brand to enter into consignment deals. Slowly and invisibly over time the ecommerce strategy transfers all inventory risk onto the brand manufacturer’s balance sheet, thus exposing the business to a centralised pure play state, but with the cost structure of a bloated traditional retail machine.

Perhaps this is what people have a hard time understanding. Pure play commerce, built on one trade level between the brand and the consumer comes across sounding very sexy with the promise of “big margin”. But, it comes with the fundamental risk accumulated in any business, and thus it must be treated very differently from the risk-distributed sales channel models of the past. In pure play, nobody shares the risk of owning inventory, and nobody has an interest in helping to source new customers. The responsibility lies whole heartedly on the brand along with a little help from brand endorsed 3rd parties like social media, SEO pop-up stores, crowdfunding and so on.

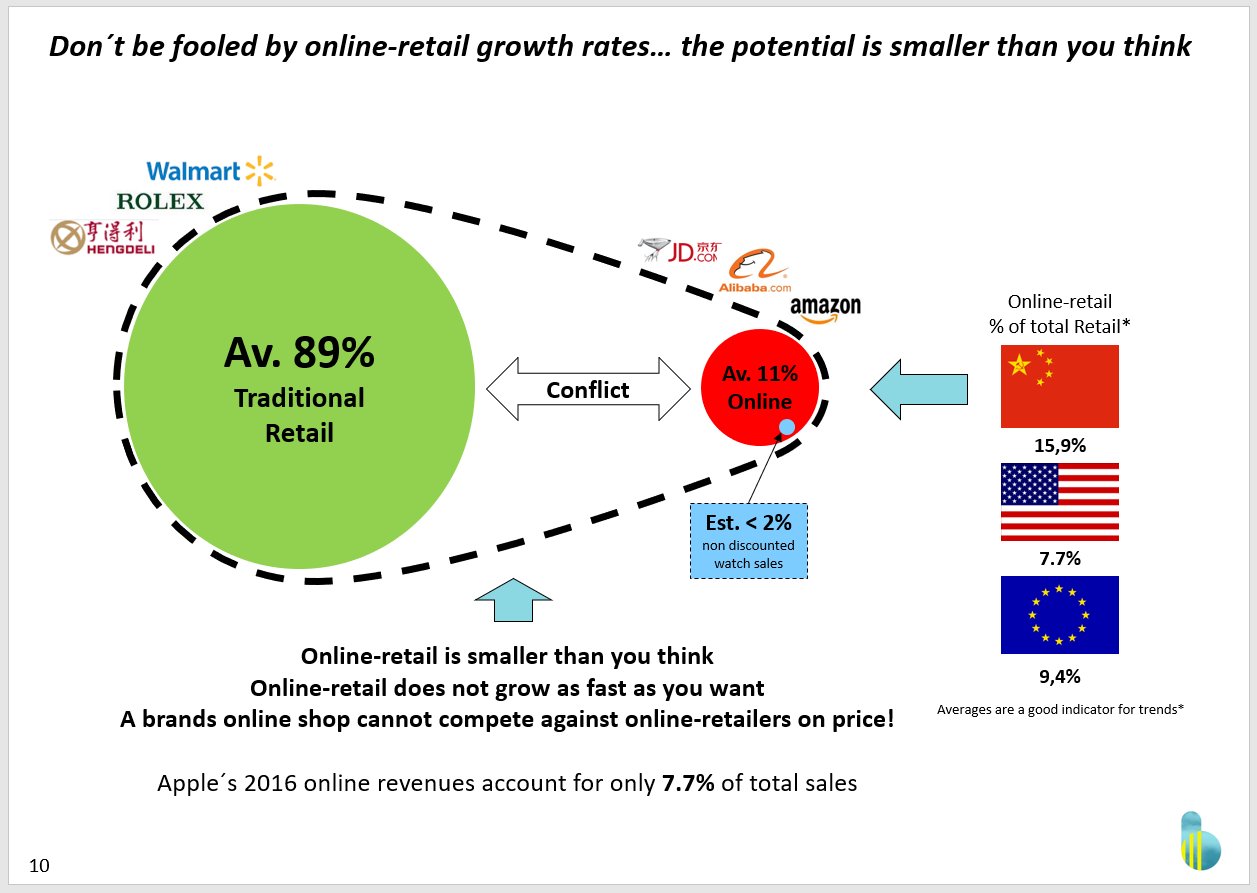

It is easy to start a pure play business, particularly with platforms like Kickstarter and I love that platform, having done several campaigns by myself. Moreover and only rarely do these start-ups survive their “post-crowdfunding-era” or continue on as a successful business. This is because the initial pure play success, fuelled by popular crowdfunding, halts the day after the campaign is completed, and then the brutal reality of commerce kicks in. A reality that tells us that global online retailing revenues represent on average 11% of retail trade, and that by 2020 this ratio will grow to about 15% of the global average… perhaps a bit more if we want to be optimistic. This means that by 2020, 85% of global commerce will likely still be going through other channels, like physical stores, malls or shop-like fulfilment places that we haven’t yet imagined.

Perhaps this is what people have a hard time understanding. Pure play commerce, built on one trade level between the brand and the consumer comes across sounding very sexy with the promise of “big margin”. But, it comes with the fundamental risk accumulated in any business, and thus it must be treated very differently from the risk-distributed sales channel models of the past.

A retailer addressing a pure play retail approach has to accept a very limited total addressable market (TAM) of only 15% for his business in 2020, in addition they face the almighty competitor Amazon that has reached a scale at which it can live with this limited accessible TAM. In order to win market share in online retailing, all you have to do is install some robots to make sure your own site always shows the best price, which is typically lower than your competitors’ and continue to do so until no margin is left and the site shuts down.

These simple numbers are something most people can easily understand. However, another truth about e-commerce is that, if you look at it from the point of view of a brand manufacturer whose primary goal is to have stable pricing to protect the brand’s image, you start to wonder how on earth an online shop run by a brand still supplying traditional retail trade is going to be able to reduce prices online. If they do have the stomach to drop their pants on price, their retailers will very soon be shouting into the phone at the head of sales. It’s understandable, and although not many people are willing to talk honestly about it, we know from some insiders in the luxury world that, if you take away grey-market online retailing, less than 1% of their business is direct pure play e-commerce.

...global online retailing revenues represent on average 11% of retail trade, and that by 2020 this ratio will grow to about 15% of the global average...

So if a 1 billion dollar luxury watch or fashion label ever decided to go pure play, their revenue would drop from 1 billion USD to less than 50 million within days😉. It is simply not possible to find success without a very stable transition strategy in place that helps the old structures morph into an integrated omni-channel world. To add more fuel to the fire, if they decide to jump into the multi-channel chaos, driven by the e-commerce community, they are likely to destroy customer loyalty as a result of consumer frustration with pricing inconsistency.

Conclusion

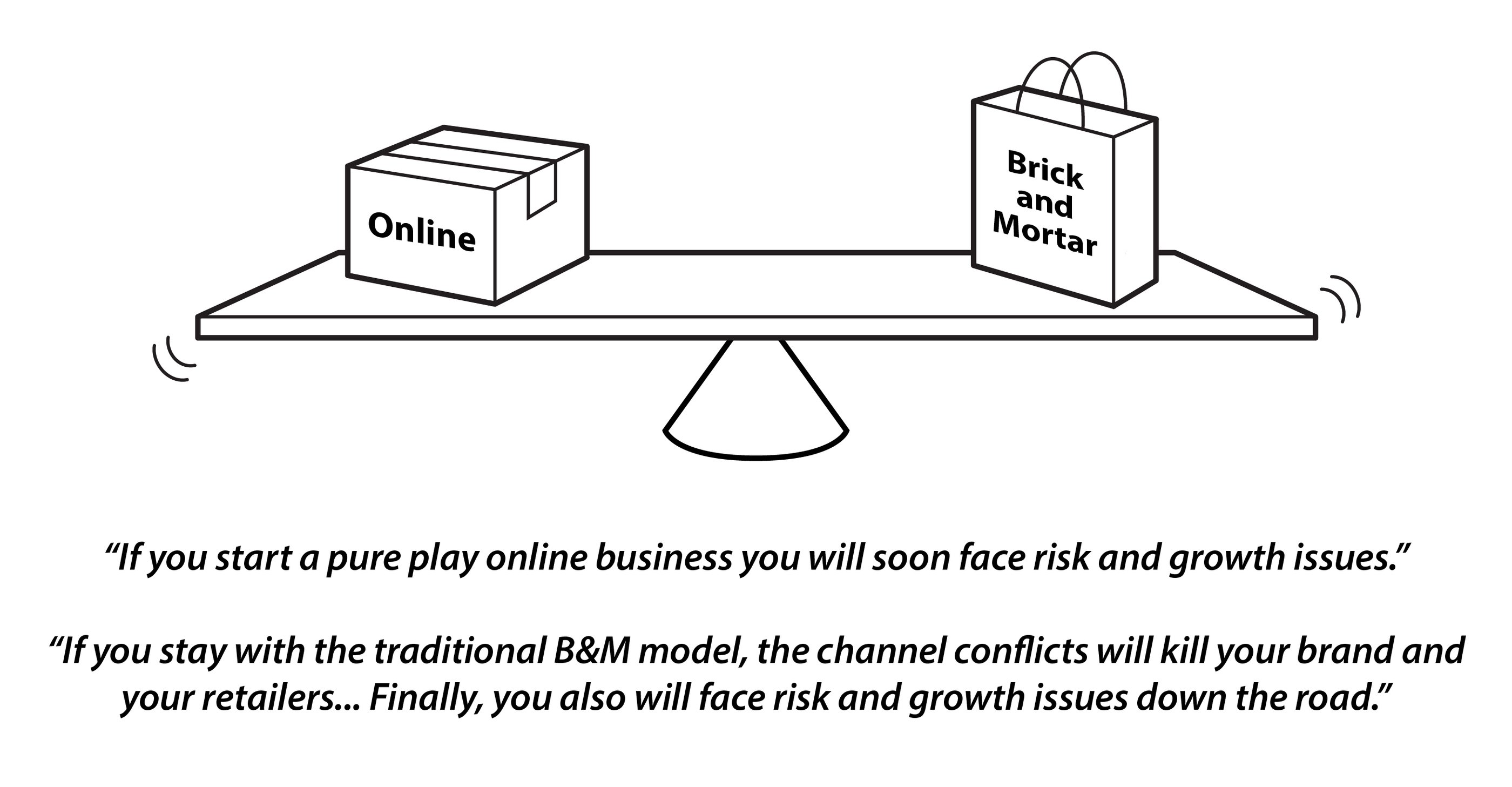

If you start a pure play online business you will soon face risk and growth issues.

If you stay with the traditional B&M model, the channel conflicts will kill your brand and your retailers... Finally, you also will face risk and growth issues down the road.

Pure play is not a true solution; because of the unpredictable risk associated with this strategy, it is therefore in most cases a myth that leads to a dead end. There is no doubt that direct brand-to-consumer business models will play an important role in the future, but getting from A to B takes time, and pure play needs to be augmented with B&M commerce, and vice versa… which brings us back to omnichannel commerce😉

As always… just a snapshot of a pretty complex matter.

Yours,

Andi Felsl

-

- Andreas Felsl – creator and thinking brain behind BrandCloud

- Andreas Felsl has founded, built and run companies in the world of mechanical watches, sporting goods and the software industry. He has among others founded the watch brand Horage. With his new project BrandCloud, he now works hard on answering the “28-trillion-dollar” question of how to reach the state of Omnichannel-Retail. A state in which there is no difference between online and offline commerce, relieving us from today’s shopping paranoia caused by commerce out of control.